Willful Blindness

What the System Knows and Chooses Not to See

A note to the reader: This essay is long - about 11,000 words, or roughly 45 minutes of reading. That’s because I’m trying to reveal a pattern that only becomes visible when you view the individual parts in context. You can easily skip the technical sections with tables and numbers - the structure is more important than the individual figures. The point isn’t to remember the percentages. The point is to see that they are interconnected.

We are at a moment when an entire system is choosing to look the other way.

On Wednesday, May 6, 2026, the S& P 500 closed at a new all-time high - driven by speculation about an impending Iran deal, as reported by Axios. That same morning, Trump had called the deal “perhaps a big assumption” on Truth Social and threatened that the bombings would resume “at a much higher level and intensity than before.” The market seized the opportunity - and soared.

Two days later, on Friday, May 8, the index closed even higher - this time driven by a jobs report whose headline “beat expectations” (115,000 new jobs versus an expected 55,000), but whose underlying data was disastrous: The labor force fell by 226,000, the participation rate dropped to 61.8% (the lowest since October 2021), and the U6 unemployment rate rose to 8.2%. The tech sector as a whole has risen +12% over 10–20 trading days (from mid-April to May 8), driven by AI euphoria. AMD’s market cap had skyrocketed by 90% in a month (from around $200–250 billion to $380–450 billion), while Nvidia rose ~50% over the same period. AMD’s stock nearly doubled over the course of five weeks, driven primarily by demand for their AI chips (MI300X).

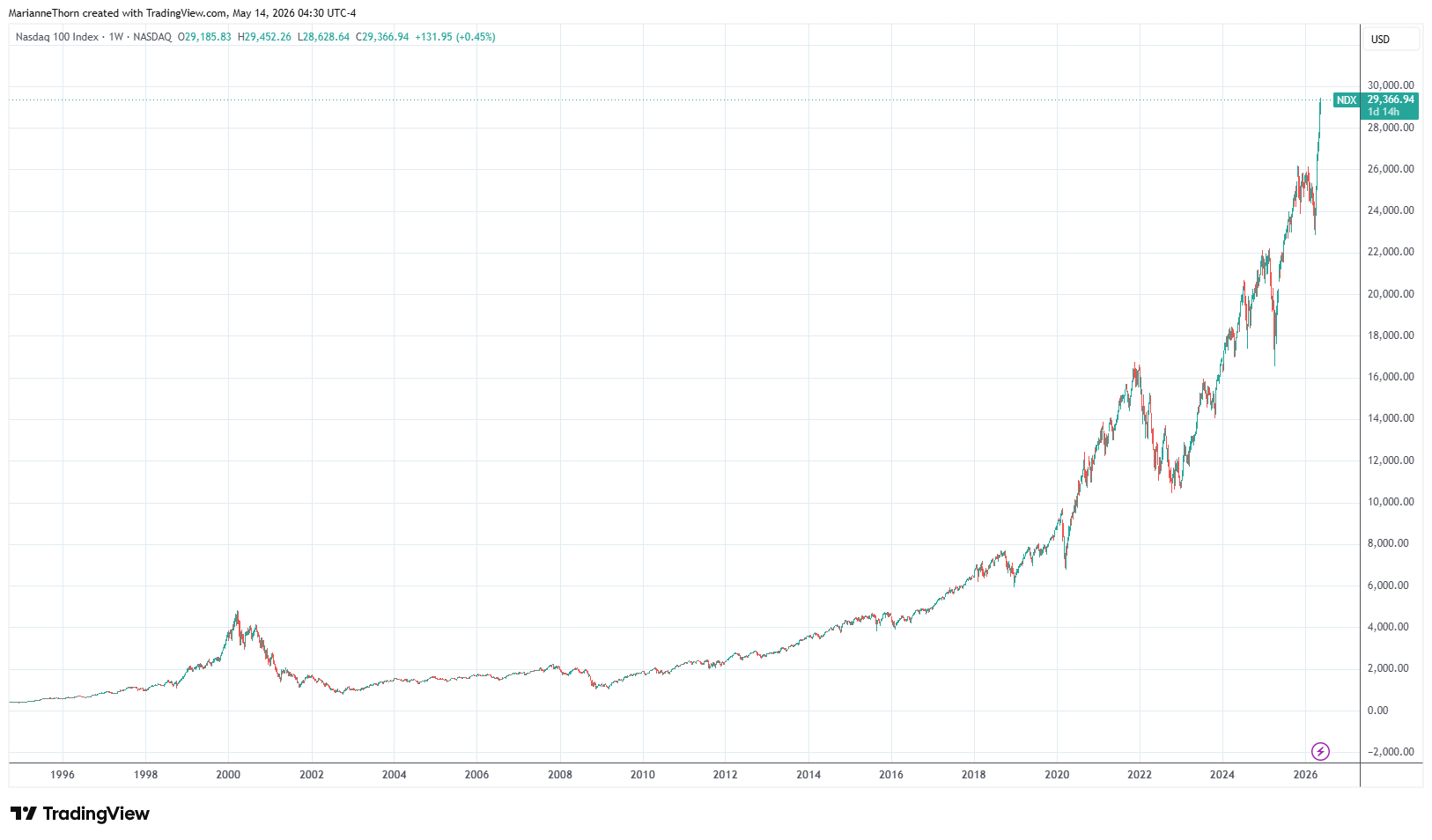

NASDAQ Composite, 1995–2026 (log scale). Three peaks, same pattern. The dot-com bubble in 2000. Pre-financial crisis 2007. And now - five times higher than the dot-com peak, driven by a handful of AI stocks whose business model relies on structural deflation of wage income. The Buffett indicator stands at 230%, compared to 146% at the dot-com peak and 109% before 2008. Source: TradingView.

That same Friday, Michael Burry - the investor who, as one of the few, saw the subprime bubble in 2005, was ridiculed for three years, and was proven right in 2008 - wrote on X: “Stocks don’t go up or down because of jobs or consumer confidence. They’re going straight up because they’ve been going straight up.” He compared the situation to the final phase of the dot-com bubble.

Three days later, on Monday, May 11, the index rose again to a new record - this time despite Trump’s rejection of the Iran deal.

Two days later, on Wednesday, May 13, the index set yet another record - the fifth in twelve days. The S&P 500 closed at 7,444.25. Apple crossed $300 for the first time ever. Nvidia set a new all-time high for the sixth day in a row. The S&P 500 added $516 billion in market value in a single day. The record was set on the same day the Producer Price Index for April was released: an increase of 1.4% - expected: +0.5% (PPI rose nearly three times more than expected) - the largest monthly increase since March 2022, and nearly three times higher than expected. That should have been bad news for the market. Instead, it became yet another record.

On the same day, the Senate confirmed Kevin Warsh as the new Fed chair by a vote of 54-45. Jerome Powell’s term expires on Friday, May 15. The last institutional resistance to the asset-price narrative that has driven the market will disappear in two days.

Five records in thirteen days. Each triggered by a different narrative. Wednesday: rumors of peace. Friday: jobs numbers that “beat expectations.” Monday: rejection of peace. Wednesday: new Fed chair.

The market ignored him. Closed its eyes. Grabbed the balloon - as it always does. Until it can no longer.

Every day has its specific trigger. But the direction is predetermined: Every day, the market finds the narrative that justifies the rise it is already in the midst of. No one listens to those who stop and ask: What does it mean when an entire financial system chooses narrative over reality - and when that is institutionalized as policy.

Trump ignores the problems - or rather: he defines them away. Ask about oil prices, and he answers: the stock market. Ask about gas, and he answers: the stock market. Ask about inflation, and he calls it “fake.” The stock market functions as a shield - a single yardstick meant to overshadow all other realities. Consumer confidence, life expectancy, delinquency rates, actual consumer behavior - everything else is dismissed.

The University of Michigan’s consumer confidence index hit 48.2 in early May - the lowest level ever in data dating back to 1946. Lower than during the inflation shock of the 1970s. Lower than during the financial crisis of 2008. Lower than during the pandemic. Trump said that same week: “Everything’s doing really well.”

This is not willful blindness in the classical sense of “we didn’t know.” It is willful blindness in its most disturbing form: A system that has chosen a single metric - the asset price - and declared it to be reality, while dismissing all other indicators as irrelevant. A system that has chosen a narrative - and called it reality. The difference is crucial. The asset price is not reality. It is a construct determined by the mechanisms we have just seen: algorithmic trend-following, information asymmetry, presidential signaling, wealth concentration among the top 10%. When this single constructed yardstick is elevated to reality, while consumer confidence at 48.2 (the lowest since 1946), credit card delinquency at 12.7%, and declining life expectancy are dismissed as “fake” or irrelevant - then we have a system that does not merely turn a blind eye to reality. It has replaced reality with a metric it can manipulate itself.

This essay is about what it means when a financial system - and the state tasked with regulating it - chooses narrative over reality. And about how the consequences of that choice extend far beyond Wall Street: to oil prices in the Philippines, to credit card debt in Ohio, to the chip supply in Taiwan, and to the refugee flows that will soon hit Europe’s shores. For when you close your eyes to one reality, you ultimately close them to all of them.

The Anatomy of Disconnection

The Market as an Amplifier of the Few’s Knowledge

A market that rises on rumors reveals more about market mechanics, power, and greed than about economics. Not because anyone believes the rumor, not because fundamental data is improving, but because the market’s own infrastructure is designed to amplify any movement in one direction.

Today, the so-called CTAs - Commodity Trading Advisors, or managed futures - manage around $300–350 billion in assets. Due to futures leverage, they typically control positions many times larger than their own capital. Goldman Sachs estimated at the end of 2025 that CTAs’ long exposure in U.S. stock index futures alone amounted to $65–70 billion.

These funds track price alone - not fundamental data. They do not read quarterly earnings reports. When the S&P 500 breaks above a certain moving average or momentum level, CTAs are forced by their own algorithms to buy. When the index falls below the threshold, they are forced to sell.

Structurally, this means: Whoever can push the price above a certain threshold doesn’t need to have the capital themselves to move the entire market. The CTAs - the algorithmic trend-followers - do the rest. You pay for the match - the trend-followers pay for the fire.

Add to this the so-called 0DTE options - options that expire on the same day - which in 2026 will account for over half of the S&P 500’s ’s options volume, an activity that was virtually nonexistent in 2020. Every time the price crosses certain levels, options issuers are forced to hedge by buying the underlying stocks, which further amplifies the movement.

Add in passive index funds, where U.S. 401(k) pensions automatically pump in about $50 billion every month - regardless of market valuations. And add retail traders who, via platforms like Robinhood, buy on every dip, because they have been conditioned by 15 years of rising markets to believe that declines are always buying opportunities.

The overall picture is a market that is structurally designed to amplify any trend. That does not mean that it always goes up. It means that it rises with ever-diminishing fundamental justification - and that it falls with ever-greater intensity once the trend reverses. The path up is long and self-sustaining. The path down is steep and self-reinforcing.

The key consequence is information asymmetry. Whoever knows when an announcement is coming - a tariff suspension, a regulatory easing, a geopolitical statement - can position themselves ahead of it. They don’t need to buy enough to move the market alone. They simply need to push the price past a publicly known CTA level. The market mechanics take care of the rest.

In April 2026, the CFTC opened an investigation into precisely this pattern. According to Bloomberg, regulators have asked the CME Group and Intercontinental Exchange to hand over Tag 50 identifiers - data that can identify the parties behind specific trades - for unusual spikes in volume immediately prior to Trump’s announcements. At least two episodes over a two-week period showed that volume in both stock index futures and crude oil futures spiked without any apparent trigger - minutes before an announcement. Senators Elizabeth Warren and Sheldon Whitehouse have formally asked the CFTC to investigate whether there has been “recurring misuse of material non-public government information.”

Whether the investigation survives the political headwinds is an open question. But the investigation itself is now on paper - and this is a rare instance of the system attempting to scrutinize itself.

The market has also internalized two phenomena that now function as permanent structures. The first is called the TACO trade - Trump Always Chickens Out - where traders have learned that his tariff threats are systematically followed by pauses or retreats, and therefore position themselves contrary to his statements. The second is the Trump put - the market’s assumption that the president will intervene against major declines because he uses the Dow Jones as his personal success indicator.

Both effects create predictable patterns that insiders can exploit - in ways that are inaccessible to ordinary investors.

This is where it becomes crucial to understand what this means for the individual American - but also for the rest of the world. Given the size, power, and significance of the U.S. to the global economy, the rest of the world can only watch as the snowball grows.

The top 10% of U.S. households own about 90% of the stock market. When the market rises, the gains go to them. The top 1% has increased its share of wealth to 32% - the highest level since the Federal Reserve began tracking it in 1989, and that equals the combined wealth of the bottom 90%. The top 0.01% - Bezos, Musk, Zuckerberg, Ellison, and their peers - have accumulated wealth so rapidly over the past 15 years that their combined holdings have now doubled compared to 2010, while the median household’s real purchasing power has stagnated. The share of wages in GDP is at its lowest level in 75 years.

When Trump therefore declares that the stock market is proof that “everything is going really well,” he is saying something that is technically correct for about 10% of the population. For the 1% who own a third of everything, things are going fantastically. For the 0.01% who have positioned themselves ahead of his announcements, things are going even better.

For the bottom half - notably 170 million people, more than ten times Denmark’s population - things are not going well. Credit card debt has reached 12. 7% delinquency, the highest since 2011. The auto finance sector is reeling with a 5.2% delinquency rate, surpassed only by the fourth quarter of 2010 during the crisis. 50% of Americans are effectively poor or on the brink of poverty. This is not a statistical curiosity. It is the simplest form of fundamental inequality: a broad American underclass living paycheck to paycheck in the country with the highest GDP per capita in the G7.

The two groups live in the same country, but in two different economies. One is reflected in the Dow Jones. The other is reflected in the University of Michigan’s consumer confidence index of 48.2, the lowest since 1946.

These are not two sides of the same reality. They are two realities whose decoupling is actively maintained by the mechanisms that determine what counts as reality. Asset prices are the tool of the top 10%. Default is that of the bottom half. Both are real. Only one counts in the official narratives.

As former Citibank trader Gary Stevenson - now one of the sharpest voices in British economic debate - has put it:

“The world of the billionaires has exploded, the world of the public sector has collapsed, and the world of the middle and working classes has collapsed. It’s the same thing. It’s a transfer of wealth.”

That is the fundamental anatomy of the disconnect: When the market rises because it rises; when the infrastructure is built to reinforce the trend; when insiders get the information first; and when the president declares asset prices to be the only reality -then it is no accident that reality is asymmetrically distributed.

It is the structure that has chosen its own winners. And the winners know it. They have built the system so that it reinforces their advantage - making it invisible to everyone else and deliberately turning a blind eye to their problems.

The Buffett Indicator: When the Market Doesn’t See Reality

The Buffett Indicator - the ratio of the stock market’s total market capitalization to U.S. GDP, which Warren Buffett himself called “the best single measure of where valuations stand at any given moment” - currently stands at around 226–230%, the highest level ever - higher than the dot-com peak (146%), higher than before the 2008 crash (109%), and nearly double the historical average of around 120%. Currently, the indicator is 2.4 standard deviations above the historical average. This is not merely an overvaluation - it is an extreme statistical deviation that typically precedes market corrections.

At the same time, government finances are showing alarming trends:

The federal deficit for fiscal year 2026 was already at $1.2 trillion as of the end of March.

According to the Congressional Budget Office (CBO), projections point to public debt reaching 175% of GDP in 2056 - a level that, historically, has been associated with debt crises in other countries.

Even more concerning are developments in the bond market: At a 2-year Treasury auction in March, the major banks that trade in government bonds (Primary Dealers), had to absorb 24% of the supply - twice as much as usual. This signals waning global demand for U.S. government debt, a sign that investors are beginning to doubt the dollar’s long-term stability.

On the household front, an even more worrying picture is emerging:

The share of credit card debt that is 90+ days past due reached 12.7% in the fourth quarter of 2025 - the highest level since 2011.

Auto loans with the same delinquency rate stand at 5.2% - the second-highest quarterly rate on record, surpassed only by the fourth quarter of 2010 during the financial crisis.

The overall delinquency rate has risen to 4.8%, the highest since 2017, driven by delinquencies among low-income earners and young people.

Total credit card debt has exceeded $1.3 trillion - an amount that exceeds Denmark’s annual GDP.

The average annual percentage rate (APR) on credit cards stands at 21-23.75%, a level that makes it nearly impossible for many households to pay off their debt.

This is the K-shaped economy in action. Asset holders - the top 10% who own about 90% of the shares - are experiencing record wealth. At the same time, wage earners without shares are experiencing a continuous deterioration of their conditions.

These two realities exist in parallel under the same national GDP figure - a statistical illusion that hides the deep inequality that has emerged.

This is the deeper observation: Asset prices are no longer signals of economic health. They have become an instrument of wealth concentration - independent of productive activity, of broad prosperity.

The market is no longer a thermometer; it is a pump that automatically shifts wealth upward while concealing the structural imbalances that undermine the economy for most people.

The mechanisms driving this have accumulated over decades:

The explosion in the money supply since 2008 - and especially during the Covid-19 pandemic in 2020 - has primarily created asset inflation, not goods inflation. The reason is that the newly created money has ended up with those who already own assets (the so-called Cantillon effect) , rather than reaching the general population.

Share buybacks - banned in the U.S. from 1934 to 1982 as market manipulation, but re-legalized by the Reagan administration - have transformed corporate earnings from reinvestment to financial engineering. Today, the average large U.S. company spends more on share buybacks than on research and development.

Tax policy favors capital income over earned income by an ever-widening margin.

According to the CBO, Trump’s Big Beautiful Bill (OBBB) adds $4.2 trillion to the federal deficit over 10 years, primarily through tax cuts that benefit top earners and large corporations.

On top of this structural foundation, the Trump administration has added a further asymmetry:

Political signaling that creates direct asset price stimuli - the creation of a strategic crypto reserve, deregulations, and tariff suspensions - combined with a weakening of the SEC’s enforcement capacity.

This is not the creation of a new phenomenon. It is a catalyzed intensification of an existing dysfunction - a dysfunction that is now playing out with greater speed and greater risk than ever before.

This is precisely MarketWorld in its purest form - the world Anand Giridharadas describes in Winners Take All.

The rhetoric that “markets generate wealth,” “low taxes create jobs,” “stock buybacks return capital to owners,” “crypto innovation democratizes finance” - all this win-win rhetoric masks a simple, but uncomfortable truth: upward wealth transfer masked as market efficiency.

When 813,000 wallets lose $2 billion on the $TRUMP memecoin, while 58 wallets gain $1.1 billion, that is not market efficiency. It is extraction - a systematic transfer of wealth from the many to the few. But the language makes it invisible - because the losers acted “voluntarily.”

Asset prices have become the central propaganda tool.

The sitting president focuses on the Dow Jones - not because the Dow reflects the economy, but because the Dow is the only number that can be presented as “success,” while all other indicators - median income, debt, mental health, life expectancy, social mobility - are deteriorating.

The stock market has become a distraction mechanism - and it functions as such precisely because it is manipulable through the mechanisms we have described. It only works because the majority of Americans do not own significant amounts of stock and therefore have no “skin in the game.” They are shown the outcome of a market in which they do not participate and asked to accept it as a measure of the nation’s health.

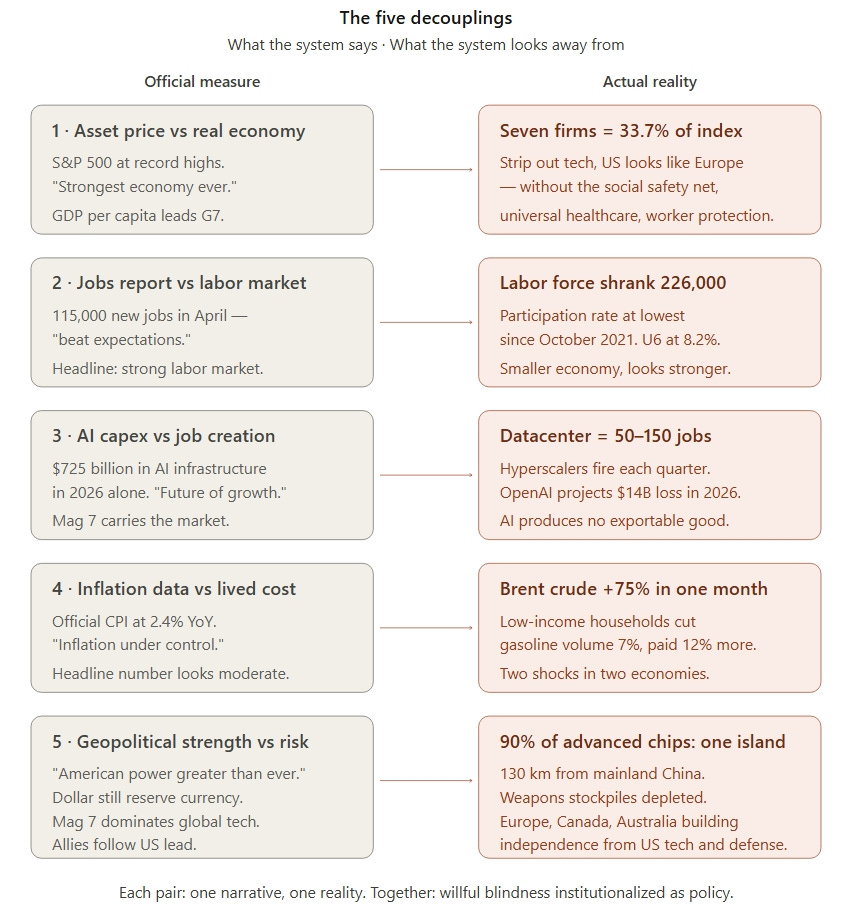

The Five Decouplings

The anatomy of the decoupling is not a single thing. It is five simultaneous movements, each documented by official institutions, each explained publicly, and each ignored in the official narrative of American strength.

The five decouplings are not independent of one another. They reinforce each other, and it is their interplay that makes the crisis greater than the sum of its parts .

The first concerns asset prices. The second concerns job numbers. The third concerns AI investments. The fourth concerns inflation. The fifth concerns geopolitical position.

Each one is its own story. Together, they tell a single story: of a system that knows better - but chooses to turn a blind eye.

Decoupling 1: Asset Prices versus the Real Economy

The seven largest U.S. technology companies - Apple, Microsoft, Nvidia, Alphabet, Amazon, Meta, and Tesla - account for 33.7% of the S&P 500’s total market capitalization in April 2026.

In 2016, it was 12.5%.

The ten largest companies together account for 39% of the index - far exceeding the dot-com bubble’s peak of 27% in 2000.

We’ve moved past 2000.

Goldman Sachs expects the seven largest companies to account for 46% of the S&P 500’s total earnings growth in 2026.

This means that 1% of the index’s companies account for nearly half of all earnings growth, while the remaining 493 companies account for the other half.

That is not a healthy economy. It is an extreme concentration - and a dangerous one at that.

The earnings concentration is even more striking:

The top 7 account for 26% of total net income in the S&P 500.

67% of the IT sector’s total earnings come from these seven companies.

These companies trade at P/ E multiples of 31 - while the rest of the market trades at 21.

At the dot-com peak, the top 10 traded at a P/E of 43 versus 21 for the rest. We are not quite at dot-com levels in terms of ratios - but we exceed the absolute concentration.

Paul Krugman - Nobel laureate in economics - documented this exact pattern on May 10, 2026, while this essay was being drafted.

Krugman’s observation is crucial because he writes from a European perspective about the U.S. economy:

In 2001, France had a GDP per capita of 74% of the U.S. level, measured in purchasing power parity.

In 2024, it was 73%.

Germany has actually closed part of the gap.

The U.S. growth advantage since 2010 - on which the entire American narrative of an “exceptional economy” rests - is largely due to the expansion of the technology sector.

If you take tech out of the equation, the U.S. economy resembles Europe’s.

Not only that: on many metrics, Europe’s economy resembles a better version of the U.S.’s.

Krugman uses an analogy worth remembering: “ In economic terms, Europe is to the U.S. as Texas is to California.”

California has grown faster than Texas since 2007 because it is home to the tech clusters. But no one in Texas feels poorer because of that. The gains from technology are distributed globally through the market for the products the tech sector delivers. The average European uses Google, buys Apple, and subscribes to Netflix. The value is produced in the U.S. The value is consumed internationally.

The next day, Krugman published a technical note formalizing the point: In a two-country model where one country dominates the rapidly growing tech sector, that country’s measured GDP grows faster - but real wages in both countries rise by the same amount. The difference in scale thus does not reflect a difference in living standards. It is a formally demonstrated scale artifact.

When you subtract the tech-generated growth out of the GDP figures, the U.S. is left with an economy that resembles Europe’s—but:

Without Europe’s social safety net.

Without Europe’s universal healthcare system.

Without Europe’s worker protections.

Europeans work shorter weeks and have longer vacations - by choice, not as a sign of underdevelopment.

Americans work longer weeks with poorer social protection, and the result is not a higher standard of living. It is longer workdays for poorer social security.

Krugman followed up on May 12 with an elaboration of the point in human terms. American life expectancy is now significantly lower than in other affluent nations - and the gap is growing every year. Infant mortality in the U.S. is higher than in some significantly poorer countries. Traffic fatalities are now far more common in the U.S. than in Portugal - the country where Krugman himself worked in 1976, where driving was terrifying, and which has since surpassed the U.S. in road safety. The murder rate is several times higher than in European cities, despite the fact that American right-wing commentators portray European cities as dangerous. The average German employee has 25 to 28 paid vacation days annually. The average American private-sector employee has 10. And the U.S. is the only industrialized country that does not guarantee health insurance to its citizens. That is the reality the GDP figure hides. That is what will erupt as political anger when the American public realizes that the narrative of “exceptional economy” was a measurement artifact - built on a figure that measures the wrong thing.

That is the first disconnect. The stock market in the U.S. does not reflect the American economy. It reflects seven companies.

Decoupling 2: Job Numbers Versus the Labor Market’s Real Strength

On Friday, May 8, 2026, the Bureau of Labor Statistics report showed 115,000 new jobs - nearly twice as many as expected.

The headline read: “Strong labor market.” The numbers below the headline told a different story.

Indicator Number Reading

New jobs created 115,000 “Beat expectations”

Expectation 55,000 Headline positive

Labor force -226,000 Contraction

Labor force participation rate 61.8% Lowest since Oct. 2021

Unemployment (U3) 4.3% Unchanged, appears stable

U6 (broad measure) 8.2% Up 0.2 percentage points

Part-time workers for economic reasons +445,000 to 4.9 million Strong growth

Real wage growth +3.6% YoY Below inflation

How can 115,000 new jobs be created while the labor force shrinks by 226,000?

The answer lies in immigration policy.

In February 2026, Goldman Sachs published an analysis of what they call “ break-even job creation” - the number of new jobs needed to keep the unemployment rate constant. In the 2010s, this figure was around 70,000 per month. Goldman now estimates that it has fallen to 50,000 by the end of 2026, due to the collapse of net immigration.

Year Net Immigration Difference

2010s (avg.) ~1 million/year Baseline

2024 2.7 million (Census)

2025 1.3 million -54% in one year

2026 (Goldman) 200,000 -80% from the 2010s

2026 (Census) 321,000 Heading toward negative

The U.S. is heading toward its first negative net migration in over 50 years. More people will leave the U.S. than arrive.

When you remove immigrants, the number of jobs that need to be created to “look strong” drops. “ This means that a jobs report of 115,000 in 2026 looks stronger than it would have in 2022. It is not a strong economy. It is a smaller economy that looks strong because the yardstick has been moved.

In May 2026, the University of Colorado Boulder published a study documenting what the ICE raids actually do. The official claim from the Trump administration: Removing undocumented workers “frees up jobs for Americans.”

The researchers found the opposite. In cities where ICE has conducted raids, employment of U.S.-born men with a high school education fell by 3% in the construction sector. When construction companies lose their undocumented workers, they don’t hire Americans. They cut back on projects. They don’t fulfill orders. They close down.

The American Enterprise Institute - a conservative think tank not known for being critical of Republicans - published a working paper in 2025 projecting that Trump’s mass deportations would reduce U.S. GDP by 2.6–6.2% over a decade. That is no small matter. It is structural damage on a scale that will take a generation to heal.

The labor market looks stable because supply is shrinking faster than demand. That is not strength. It is contraction masquerading as stability.

Decoupling 3: AI Investment versus Job Creation - and the Question of What AI Actually Produces

By 2026, the four largest U.S. technology companies - Amazon, Alphabet, Microsoft, and Meta - will spend approximately $725 billion on AI infrastructure.

Company 2026 Capex (bn USD) Free Cash Flow Change 2026

Amazon 200 -17 to -28 bn (negative)

Alphabet 175-185 -90%

Microsoft 120-190 -28%

Meta 115-145 -90%

Total ~$725 billion Historic erosion of FCF

By comparison, Denmark’s total GDP is around $400 billion. Four U.S. companies spend nearly twice as much on AI infrastructure in a single year as Denmark produces in an entire year.

The question is: What are they actually building?

A large AI data center employs 50-150 full-time staff after commissioning. The construction phase generates 1,000-3,000 temporary jobs over 2-3 years, but these are temporary positions. Traditional industrial investment at the same level creates 3 0-50 times more full-time jobs per dollar invested.

At the same time, these same companies are laying off employees. Microsoft, Meta, Google, and Amazon have laid off thousands of employees every quarter throughout 2024 and 2025. The justification - which has become standard in press releases - is “streamlining” and “adapting to AI.” Investors reward this. Stock prices rise with every round of layoffs.

That is the inherent contradiction. AI investment only makes sense if it eliminates jobs downstream. Microsoft isn’t selling AI to companies because companies want more employees. They sell it because companies want fewer. Sales are measured in saved labor costs. The business model presupposes structural deflation of wage income in precisely those sectors that today support the American middle class - office work, administration, law, accounting, customer service, programming, and parts of the medical field.

It is Henry Ford’s paradox in the 21st century. When Ford doubled his workers’ wages in 1914, the argument was not philanthropic. It was economic. “If my employees can’t buy my cars, there is no market.”

The hyperscalers’ current model does the opposite. It optimizes for short-term revenue by making customers’ customers less able to have workers as customers. If companies’ customers no longer have wage income, the companies have no customers. This is not a side effect . It is the inherent contradiction.

Daron Acemoglu and Simon Johnson have documented in Power and Progress that AI technology can be developed in two fundamentally different directions:

Automation - where the machine replaces humans.

Augmentation - where the machine enhances human capacity.

Both are technically possible. Both have existed side by side throughout industrial history. The difference between them is not technical - it is political, driven by tax policy (favoring capital over labor), labor market regulation (or the lack thereof), and the hyperscaler monopoly’s profit logic.

The current choice is clear: automation.

The hyperscalers’ free cash flow reflects this. The largest and richest companies in world history are burning through cash at a rate historically seen only in companies at risk of bankruptcy. It only works as long as investors believe that AI revenue will materialize.

That belief is already wavering.

OpenAI - the company that defines the entire AI - projects a loss of $14 billion in 2026. Sam Altman has publicly admitted that the company is losing money on even its most expensive product: ChatGPT Pro at $200 a month. “We are currently losing money on OpenAI pro subscriptions,” he wrote on X in January 2025. “People use it much more than we expected.”

CFO Sarah Friar hinted in a comment (which was quickly retracted) that OpenAI was considering asking the U.S. government for a “government guarantee” - (backstop) - for its investments in computer infrastructure. Tom’s Hardware analyses project that OpenAI will run out of cash in mid-2027, unless new sources of funding are found.

This is not a marginal business. It is the central player in the entire AI narrative. Every time someone talks about “AI will replace jobs,” they are implicitly referring to OpenAI’s technology. If OpenAI cannot pay its own bills, if Microsoft, Google, and Meta are burning through hundreds of billions on data centers that do not produce physical goods that can’t be sold at a price that covers the costs - then what have we built?

AI isn’t an industry like steel production or car manufacturing. It doesn’t produce goods that can be exported. It produces computing power that is used once and then disappears. Every ChatGPT query costs OpenAI money in the form of electricity and chip wear and tear. Scaling exacerbates the problem - more users mean more losses, not more revenue.

And at the same time, four companies are burning through $725 billion to build more of it.

If the AI bubble bursts - if investors suddenly ask where the money is being made - it’s not just stock prices that will fall. It’s the entire investment flow that has propped up the U.S. stock market since 2023. The Mag 7 accounts for 33.7% of the S&P 500. If these companies have to scale back their capex plans, if Amazon can no longer justify spending $200 billion annually on data centers, if OpenAI goes bankrupt or is bailed out by the government - the narrative that underpins the entire market will collapse.

And the American middle class, which has seen no productive jobs created by AI investment - only layoffs - will be left with pensions tied to Mag 7 stock prices. This is the deepest form of collective blindness: an entire economy tied to an industry that cannot earn back its own money.

Decoupling 4: Inflation and Energy Data versus Real-Life Experience

The official CPI for January 2026 was 2.4% year-over-year. The figure looks moderate. It is not moderate.

In October and November 2025, the longest government shutdown in U.S. history took place, and the BLS had to extrapolate the CPI figures from incomplete data. Those figures are now part of the time series’ foundation. What inflation “actually was” during those months, no one will ever know for sure.

Between February and March 2026, Brent crude rose from $72 per barrel to $126.

That is the largest monthly jump in over 50 years.

The IEA called it “the largest supply disruption in the history of the global oil market.”

Gasoline prices in the U.S. have risen by $1.16 per gallon since the war began.

Jet fuel has risen 95%.

In Canada, prices have risen 30%.

These increases are not distributed evenly across the population. In May 2026, the Federal Reserve Bank of New York published an analysis of consumption patterns that documents the K-shaped consumption in figures:

Income Group Volume Consumption (Gasoline) Increase in Expenditure (in dollars)

Under $40,000 -7% +12%

Over $125,000 -1% +19%

Low-income earners cut their gasoline consumption by 7% in physical volume but spent 12% more in dollars. They can no longer afford to drive, but what they do drive costs more. High-income earners cut consumption by only 1%, while their total spending on gasoline rose 19%. They drive as before. They just pay more.

The inflation shock is not a single shock. It is two shocks in two different economies.

The real purchasing power of the average American household is falling because average wages are rising 3.6% year over year, while experienced inflation - especially for food, energy, transportation, and housing—is rising faster.

For the top 10% who own assets, wealth is accumulating faster than inflation. For the bottom 50%, there are no assets to accumulate. There are only wages, which aren’t keeping up.

Decoupling 5: Geopolitical Position versus Real Vulnerability

The fifth and deepest decoupling is the one upon which the entire argument of this essay is based. It is the decoupling that ties the other four together.

The U.S.’s strategic position in 2026 is fundamentally more fragile than the rhetoric suggests.

Weapons stocks are depleted following the conflicts in Ukraine, Israel, and with the Houthis and Iran. During the Iran conflict, the U.S. has fired missiles and ammunition worth over $12 billion.

THAAD, Patriot, Stinger, Javelin, and GMLRS stocks are all severely depleted.

Strategic oil reserves have been heavily tapped.

Treasury auctions show weakness: Primary dealers absorb 24% of 2-year notes, double the usual amount - a signal of waning international demand for U.S. debt.

In January 2026, we saw the “Sell America” trade, where the dollar, Treasury bonds, and stocks all fell simultaneously - these are behavioral patterns traditionally seen in emerging markets, not in a reserve currency.

But the most significant vulnerability concerns Taiwan. This is where the entire decoupling comes together into a single picture.

TSMC in Taiwan produces over 90% of the world’s chips under 5nm. It is the only foundry in the world currently mass-producing 3nm chips, and will be the only one at 2nm when that technology matures. By comparison, China cannot yet produce chips under 7 nm.

Nvidia, AMD, Apple, Google, Amazon, Microsoft, Meta - none of them have their own advanced manufacturing facilities. They design chips. TSMC manufactures them.

The entire $725 billion in U.S. AI investment in 2026, the entire concentration of asset prices, the entire dominance of the Mag 7 in the S&P 500 - all of it rests on a single supply chain from a single island located 130 kilometers from the Chinese mainland.

In April 2026, Foreign Affairs published the essay “The Real Threat to Taiwan: America Is Preparing for the Wrong Kind of Crisis.”

The argument is that U.S. strategy is focused on the wrong threat scenario. The U.S. is preparing for an invasion. The real risk is quarantine.

Beijing’s diplomatic framework is consistent: Trade can continue freely as long as specific conditions are met - no U.S. weapons to Taiwan, no dual-use components, no military advisers, and restrictions on exit permits for TSMC process engineers (many of whom are Chinese citizens).

Beijing does not need to invade Taiwan to control TSMC. It just needs to make it difficult for the people who know how to run the factories to leave the country.

That is precisely the scenario to which the U.S. is structurally unable to respond. You cannot intervene militarily against an export control rule. You cannot bomb a bureaucracy.

When Foreign Affairs recommends a core coalition between the U.S., Australia, Canada, Japan, and the UK - which together account for over a third of global GDP and nearly half of the global defense budget - it is a strategy that requires those alliances to function.

The Trump administration has, throughout 2025 and 2026, systematically undermined every single one of them.

The deepest contradiction is this: The leaders of the hyperscalers - Pichai, Nadella, Zuckerberg, Bezos, Huang - have all privately visited Trump in 2025, have all contributed to his inauguration fund, and have all publicly expressed support for his policies. At the same time, every single one of their companies’ business models is existentially dependent on ongoing access to Taiwan-produced silicon.

Every dollar of U.S. AI investment generates revenue for a company on an island the U.S. may not be able to protect. The AI The AI bubble is not only financially vulnerable. It is strategically self-defeating.

One must assume that there is no strategy - or that it is so ill-conceived that the absence of a strategy would be the best-case scenario. If you think the current energy crisis is bad, it is nothing compared to a crisis of chip supply. Every office, every car, every hospital, every bank, every military unit in the Western world will feel it within weeks.

If someone twenty years from now is asked to explain what willful blindness was, they will point to Taiwan. The U.S. administration spent $725 billion in 2026 on infrastructure that was existentially dependent on continuous access to advanced chips from Taiwan. At the same time, that same administration dismantled the diplomatic, military, and institutional structures that would be necessary to defend Taiwan.

They did it publicly. They did it on the record. They did it with full knowledge of the underlying dependency - because it was described in every quarterly report from every hyperscaler, in every Foreign Affairs essay, in every internal briefing from the intelligence agencies.

Capture: Who Built the Blindness

It is tempting to read current events as an anomaly. As if Trump is a deviation, a temporary break with an otherwise functioning American tradition. As if the system can return to its former state once he is gone.

That is not correct. Trump is not the disruption. He is the culmination.

Reagan began the deregulation of the financial sector. Trump is completing it. These are two sentences that span four decades. Krugman has documented it from another angle: The U.S. began to fall behind other affluent nations in health, safety, and life expectancy around 1980 - precisely when the Reagan administration took office. This is not a coincidence. It is the same pattern viewed from two different perspectives.

These are two sentences that span four decades, and they are the most important analytical tool in this entire essay. What we call Willful Blindness in 2026 is not an acute condition arising under the current administration. It is the cumulative result of deliberate political choices made by Democratic and Republican administrations since 1981. It is built by people whose names we know, whose careers are publicly documented, and whose ideological frameworks are printed in books that sit on the shelves of university libraries.

Let’s see how.

The Revolving Door: When Power Shifts from Government to the Private Sector

Robert Rubin went from being co-chairman of Goldman Sachs to Clinton’s Treasury Secretary in 1995. As Treasury Secretary, he was the chief architect behind the repeal of the Glass-Steagall Act - the 1933 law that had separated commercial banking from investment banking for 66 years, enacted as a direct response to the financial crisis of 1929. When Rubin left the Treasury in 1999, he became a director at Citigroup - the first major U.S. bank able to combine the two forms of banking, precisely because the law he had repealed no longer stood in the way. He received over $120 million in compensation over the next decade. In 2008, Citigroup was bailed out by the U.S. government using taxpayer money.

Hank Paulson came from Goldman Sachs as CEO and became Bush’s Treasury Secretary in 2006. As Treasury Secretary, he designed the TARP bailout - a package authorized for up to $700 billion - that directly benefited Goldman Sachs.

Tim Geithner was President of the New York Fed during the financial crisis and became Obama’s Treasury Secretary. After his time in government, he became president of the private equity firm Warburg Pincus.

Steven Mnuchin went from Goldman Sachs to becoming a hedge fund owner who profited from the subprime collapse, and then became Trump’s Treasury Secretary during his first term. Three months after he left office, his new private equity firm received two billion dollars from Saudi Arabia.

Janet Yellen was Chair of the Federal Reserve and subsequently became Biden’s Treasury Secretary. Between those two roles, she received $7 million in speaking fees from Wall Street banks.

Scott Bessent, Trump’s second-term Treasury Secretary, was a hedge fund owner and Soros veteran.

These are not anomalies. This is the recruitment pattern. For forty years, the Treasury Department has been staffed by people whose professional and financial lives, both before and after government service, have been defined by the financial sector.

The argument is always that expertise is needed - people who view the world through the lens of the financial sector and who serve the financial sector’s interests before, during, and after their time in government.

The British mirror image is identical:

David Cameron earned £10 million within a year of leaving the office of Prime Minister.

Tony Blair is now a consultant for Saudi Arabia, Kuwait, JPMorgan, and Sergei Brin.

Rishi Sunak’s father-in-law is one of the richest men in the world.

Gary Stevenson, the former Citibank trader who is now one of the sharpest voices in British economic debate, has put it this way:

“We’re not stupid because the people who set tax policy work for them. It works a hell of a lot for them.”

Larry Summers: the perfect example

If you want to understand what capture is and how it works, Larry Summers is the perfect example.

As Clinton’s Deputy Treasury Secretary - and later Treasury Secretary - Summers was the chief architect behind two legislative moves that fundamentally changed the U.S. financial sector:

The repeal of the Glass-Steagall Act in 1999 - the law that had separated commercial and investment banking since 1933.

The Commodity Futures Modernization Act in 2000 - the law explicitly prevented the regulation of derivatives, including the credit default swaps that later destroyed AIG and were central to the 2008 crash.

Brooksley Born, then chair of the Commodity Futures Trading Commission, attempted in 1998 - two years before the law was passed - to warn of the risks. She proposed regulating the then-nascent market for over-the-counter derivatives and was met with massive resistance from Summers, Rubin, and Alan Greenspan. Summers personally called her and pressured her. She was forced out of her job.

Ten years later, the very market she wanted to regulate collapsed, costing the global economy at least $15 trillion.

Summers was not fired. He was promoted to lead Obama’s economic response to the crisis he had helped create.

Between his time in Clinton’s Treasury and his return under Obama, Summers earned:

$5.2 million from the hedge fund D.E. Shaw over 16 months.

$2.7 million in speaking fees from Goldman Sachs, JP Morgan, Citigroup, and Lehman Brothers in 2008 - the year the financial crisis erupted.

When he stepped in as Obama’s National Economic Council director in 2009, he was the chief architect of the bank bailouts that funneled hundreds of billions of dollars to the very institutions that had paid him.

He has never been prosecuted. He has never been removed from the public sphere. He still appears as an authoritative commentator in the financial press. His only public admission of error came in 2014, in the passive voice, without naming his own role: “Financial deregulation may have gone too far.”

This is a prime example of capture. Not corruption in the classical sense - he has not received envelopes under the table. He has received speaking fees for speeches, salaries for work, and consulting fees for advice. Every single transaction is legal.

The cumulative effect is that a man, whose entire career has been funded by the financial sector, has shaped the rules under which the financial sector operates, across multiple democratic presidencies. And when he speaks about monetary policy - as he often does - he is presented as a neutral economist.

If you look at it from the perspective of current law, he is not corrupt.

Cognitive Captivity

It’s not just money. It’s language.

If your entire education is grounded in a single theoretical framework - efficient markets, rational expectations, monetary neutrality - and your professors are funded by think tanks like Hoover, AEI, Brookings, which in turn are funded by donors from the financial sector, and your colleagues move in and out of the same institutions, and your career prospects depend on being quoted by the Wall Street Journal and Bloomberg - then you are not corrupt when you argue for deregulation. You believe in it. It is the only language you know.

What philosophers call epistemic capture - cognitive captivity - is perhaps the most important concept for understanding how an entire generation of economists and policymakers could consistently advocate for policies that systematically transferred wealth upward, while sincerely believing they were serving the public good.

Larry Summers has probably never thought of himself as corrupt. He has probably thought of himself as intelligent, pragmatic, and market-respecting. His mind is not empty . It contains only one language.

In my professional life, I have met several economists who see nothing wrong with pushing the limits - or doing something that the rest of us consider morally questionable. They do so on the grounds that it is not illegal. That is why they do it, regardless of the immorality.

This is Arendt’s point about clichéd language as a substitute for thinking, applied to the modern economic elite. Decision-makers cannot see certain alternatives because those alternatives do not exist within their conceptual framework.

When Anand Giridharadas documents in Winners Take All how the language of MarketWorld - win-win, stakeholder capitalism, doing well by doing good - has colonized the entire philanthropic and political discourse, he is not describing rhetoric. He is describing how the boundaries of thought are shifted so that certain actions become unthinkable before they become politically impossible.

Those who can no longer say “tax” without saying “burden” can no longer think of taxes as public funding. Anyone who can no longer say “regulation” without saying “burden on growth” can no longer think of regulation as protection.

Language has preceded policy. Policy follows language.

The structural form: who has access

The Federal Reserve has a “Federal Advisory Council” consisting of twelve bank representatives who meet with the Fed’s Board of Governors four times a year. There is no equivalent council for workers, consumers, or borrowers.

The Fed’s economic models do not include distribution. They have GDP, asset prices, inflation. How money is distributed, who bears the costs, who reaps the gains - that is not part of their mandate or the model. It is not a mistake. It is a political choice about what counts as “the economy.”

The banks have a large apparatus of lobbyists, lawyers, and PR people in Washington. Consumer groups and labor unions have a fraction - and certainly not the same financial resources at their disposal to influence elected officials.

When a regulator considers a new rule, it receives 200 detailed analyses from industry and 5 from civil society. That skew in information is in itself a form of capture. It is not immediately about regulators refusing to listen. It is about the fact that the only information reaching them in sufficient quality and quantity comes from one side.

Federal Reserve Under Pressure

The most profound institutional change under the Trump administration came on Wednesday, May 13, 2026, while Trump was in Beijing. The Senate confirmed Kevin Warsh as the new Fed chair by a vote of 54 to 45. He succeeds Jerome Powell, whose term expired on Friday, May 15, after eight years at the helm.

Powell - appointed by Trump himself in 2018, reappointed by Biden in 2022 - has pursued a tight monetary policy since 2022 to combat inflation. He has resisted public pressure from the Trump administration throughout 2025 and 2026. He has kept interest rates higher than Trump wanted. He was the last remaining institutional brake on the asset price narrative.

Warsh is not Powell. He is a former Fed board member under Bush, has publicly criticized Powell’s tight policy for two years, and has signaled a willingness to lower interest rates more quickly - exactly what Trump wants. He is not a traditional technocrat Fed. He is the Trump Fed.

For seven decades, the Federal Reserve’s independence has been a cornerstone of U.S. economic stability. It was established following the experiences with politically controlled monetary policy in the 1930s and 40s. It was maintained through Watergate, through the stagflation of the 1970s, through the 2008 crisis. Every single U.S. president since Truman has respected it - at least publicly.

Trump does not respect it. Throughout his presidency, he has treated the Fed as a political opponent standing in the way of his asset price narrative. With Warsh, he has now secured the person - and presumably the power - he desires.

The last remaining independent institution capable of curbing the asset price bubble is being dismantled. The ECB in Frankfurt will remain independent. The Bank of England will remain independent. But the Federal Reserve - the central banking system that controls the world’s reserve currency - will, starting Monday, May 18, May, be under direct presidential pressure.

The consequence is that the feedback mechanism that has kept U.S. inflation in check will disappear. If Warsh lowers interest rates faster than the underlying economy allows- and that is precisely what he has been appointed to do - the result will be higher inflation, lower real wages, and even greater asset price concentration.

This is precisely the pattern this essay has described - now accelerated by the very institution that could have slowed it down.

Reagan did not start this. Trump is completing something that has never existed before: a U.S. central bank that can no longer resist political pressure.

Slobodian: Enclosure as a Project

Quinn Slobodian has documented in *Globalists* how the neoliberal project - from its beginnings in 1930s Geneva (with Hayek, Mises, Röpke) - was never about “free markets” versus “states.” It was about isolating the market from democratic pressure by creating supranational structures that made national tax policy structurally difficult.

Hayek himself called it the “encasement” of capital against what he termed “unlimited democracy.” The WTO, EU competition law, ICSID investor protection, international tax treaties, free trade agreements. Each instrument is a layer in that encasement, making it harder for a democratic majority to tax, regulate, and redistribute.

What we now call capital flight is not a marginal evasion of the system. It is the system’s original intent unfolding.

In his recent book Crack-Up Capitalism, Slobodian has documented the next phase: Special Economic Zones, Charter Cities, free ports, digital sovereign jurisdictions (Dubai, Singapore, Honduras’ ZEDE project, Próspera, Peter Thiel’s seasteading experiments).

He calls it “the secession of the wealthy from the territorial state.”

When Bezos builds his fortune in Washington State using the state’s schools, infrastructure, legal system, and research networks, and then moves to Florida to avoid the state’s wealth tax, it is not a marginal choice. It is the central logic of how modern fortunes work: build under one jurisdiction, be taxed under another, and keep the two from intersecting. Wealth is far easier to move than earned income.

Crypto: Enclave in its purest form

The most profound example of Slobodian “encapsulation” in the current administration is not a free port or a charter city. It is crypto regulation - or rather: its systematic dismantling.

In January 2025, Trump signed an executive order establishing a strategic crypto reserve consisting of Bitcoin, Ethereum, XRP, Solana, and Cardano. In March 2025, the SEC under the new leadership, the SEC dropped a number of pending lawsuits against major crypto platforms. Coinbase, Binance, Kraken - all cases dismissed. The so-called “Crypto Czar” David Sacks - a Silicon Valley investor and personal friend of Trump - now leads the administration’s crypto policy.

It is not just deregulation. It is something more fundamental.

The crypto infrastructure - in the form it is now evolving under U.S. law - is a payment system that, by design, evades government control. Transactions can take place pseudonymously. Value can be moved across jurisdictions without passing through a regulated financial institution. Smart contracts can execute financial agreements without intermediaries. Stablecoins - digital tokens pegged to the dollar - can operate as a parallel currency without Federal Reserve oversight.

Each of these features is presented as “innovation” and “the democratization of finance.” The actual effect is quite different. Crypto does three things at once, all of which systematically weaken the state’s capacity to regulate capital:

First: It makes tax enforcement structurally more difficult. The IRS can, in principle, require reporting of crypto transactions, but in practice, pseudonymous transactions on decentralized platforms are nearly impossible to track in real time. When Bezos wants to move $100 million to a foreign jurisdiction, it requires lawyers, banks, and paperwork. When a dollar is converted to Bitcoin and sent to a wallet with no named owner, it requires nothing.

Second: It makes sanctions and cash flow control structurally more difficult. The SWIFT system remains the dominant infrastructure for international payment processing, and SWIFT is subject to U.S. and European regulation. Crypto is not. Iran, North Korea, Russia - all have experimented with crypto infrastructure to circumvent sanctions. It is technically difficult, but it is not impossible, and it is getting easier every year.

Third: It creates a parallel currency that is not subject to central bank policy. When USDC and USDT - the two largest stablecoins - combined have a market value of over $200 billion (2026) and circulate on platforms outside the Federal Reserve’s direct oversight, we effectively have a shadow dollar operating without the stabilization mechanisms that the official dollar has. If a major stablecoin collapses - like TerraUSD in 2022 (a loss of $40 billion) - the losses could be enormous, and there is no “lender of last resort.”

The $TRUMP meme coin, where 813,000 wallets lost $2 billion while 58 wallets gained $1.1 billion, is not a curiosity. It is a harbinger of what unregulated crypto trading means for ordinary Americans. It is precisely the kind of extraction - from the many to the few - that this essay has described. But now carried out with a speed and opacity that have never existed before.

The point is not that crypto itself is the problem. The point is that, under current legislation, crypto becomes an instrument that makes taxation, sanctions, and financial stability policy structurally more difficult. It is Slobodian’s “enc asement” made digital. It is the separation of capital from the territorial state, executed with code instead of jurisdictions.

The Trump administration sells it as technological progress. The actual effect is that the instruments a democratically elected state can use to regulate capital are becoming less effective year by year. This is not a side effect. It is the strategy.

Buy, borrow, die

The modern financial elite has devised a technique that renders traditional taxation analytically obsolete. In the old days, the wealthy accumulated wealth and then sold it to finance consumption or inheritance. Each sale triggered capital gains tax. The tax system was built around the assumption that the wealth would sooner or later pass through the point of realization, where the state could take its share.

The modern strategy avoids this entirely. Bezos does not sell Amazon shares. He pledges them as collateral. When he needs liquidity - for a wedding in Venice, for the acquisition of the Washington Post - he borrows against his stock holdings. The loan is not taxable because, legally, loans are not income. He pays interest that is minimal relative to the ongoing growth of his wealth. When he dies, his children inherit the shares with a “stepped-up basis” - the original purchase price is reset to the market value at the time of death, eliminating any capital gains that ever existed.

The technique is called “buy, borrow, die.” It is not a marginal manipulation. It is the dominant principle of capital accumulation among the top 0.01% of American and British society. Larry Ellison has borrowed billions against his Oracle holdings. Elon Musk pledged 90 million Tesla shares in 2022 alone. The Walton heirs, the Murdoch family, the Koch brothers - same pattern.

In 2021, ProPublica revealed IRS data documenting that between 2014 and 2018, the 25 richest Americans paid an average effective tax rate of 3.4% on their total wealth growth:

Bezos: 0.98%

Musk: 3.27%

Bloomberg: 1.30%

Buffett: 0.10%

The average American pays about 14% of their annual income in federal taxes alone.

Gabriel Zucman and Emmanuel Saez have documented that the 400 richest American households now pay a lower effective tax rate than the lower middle class. This is not a calibration error in a progressive system. It is reverse progressivity, made permanent through forty years of deliberate policy.

It is - to borrow Stevenson’s term - heredocracy, not capitalism. The outcomes for individuals, especially for younger generations, now depend on the size of the inheritance they receive from their parents. Those who do not inherit no longer have the opportunity to build wealth through work. Those who inherit no longer need to work.

Pillar Two: the blocked countermeasure

It has not been impossible to act. In 2021, 142 countries signed the OECD/G20 agreement on Pillar Two - a global minimum tax of 15% for large multinational corporations. It was the first serious attempt at international tax coordination in half a century. Gabriel Zucman, who has led much of the analytical work behind the agreement, has also proposed in 2024 a global minimum tax rate of 2% for billionaires, which would generate up to $250 billion annually.

Brazil, France, Spain, South Africa, and Germany supported the proposal. The U.S. and the U.K. rejected it.

In January 2025, the Trump administration declared that the U.S. would no longer implement Pillar Two. It threatened retaliatory measures against countries that imposed the minimum tax on U.S. companies.

The EU has stood by the principle but is under massive pressure. The UK has signaled a willingness to “modernize” its implementation - the kind of phrasing that, in diplomatic language, means phasing it out. The UK might well need to reconsider, given its economic situation.

If Pillar Two falls, 2025-2026 will be remembered as the point at which the last serious attempt at multilateral reform was crushed. It will be no coincidence that this happened under a U.S. administration whose economic team is staffed by people who have profited from precisely the offshore structures that Pillar Two was intended to target.

Piketty’s Diagnosis

Thomas Piketty has documented the deep historical dynamics. When the rate of return on capital (r) exceeds economic growth (g), existing wealth grows faster than new earnings, and society moves structurally toward inheritance-based wealth concentration.

Piketty has documented that r > g has been historically normal in all societies except for the extraordinary period between 1914 and 1970, when the world wars, the Depression, and high postwar tax rates kept the opposite relationship (g > r) in effect.

Share of wealth income in GDP:

1900-1910: 35-40%

1950-1970: 20-25%

2026: 30-35%

We are heading back to the structure of La Belle Époque - a period when a family’s surname meant more than a person’s work, when social mobility was the exception rather than the rule, when most people were born into a place they could not leave. Like the Indian caste system. Like Europe’s Middle Ages.

The modern American middle class - the postwar generation that could buy a house, send its children to school, retire - was not capitalism’s natural state. It was a historical anomaly, made possible by the destruction of existing wealth during the world wars and by postwar tax rates that kept wealth concentration in check.

When Reagan began to roll back those tax rates in 1981, he opened what Stevenson calls Pandora’s box: permission for a class of people to aggressively increase their share of wealth.

The deeper point: Capture is infrastructural

Capture has not been merely intellectual. It has been infrastructural.

Every time a regulatory agency has been weakened - Glass-Steagall, the CFTC, the SEC, the FCPA - it has made future reform more difficult. Every time a tax loophole has been expanded - stepped-up basis, carried interest, offshore structures - it has made taxing the wealthiest more technically difficult. Every time an offshore jurisdiction has been allowed to develop without consequences, it has made capital flight easier. Every time international tax coordination has been watered down, it has made collective action less likely.

The accumulation of capture effects over four decades means that the window in which reform was still technically possible is closing. It is not merely that the will is lacking. It is that the capacity has been actively dismantled. It is this difference that makes 2026 more serious than 2008.

In 2008, the financial crisis broke out, and the response apparatus functioned. The Federal Reserve, the Treasury, Congress, the FDIC, international central bank cooperation - all intact. The crisis got ugly. The banks were saved. Homeowners were not. But the capacity to act existed.

In 2026, that capacity is actively being dismantled:

The Treasury is headed by a hedge fund owner.

The Federal Reserve is under direct presidential pressure.

SEC enforcement has been weakened.

FCPA enforcement is suspended.

The Public Integrity Section at the DOJ has been reduced from 36 to 2 lawyers.

Those who are now removing the inspectors general have simply completed the work their ideological forebears began at the Treasury under Clinton. The difference is not direction. The difference is that the previous generation still felt the need to justify their actions using market-theoretical language. The current generation has abandoned that justification. They are removing the rules because it serves their interests to do so, and because there is no longer a power that can stop them.

Reagan began it. Trump is completing it.

It is not a break. It is a continuum.

The Butterfly Effect: The Absence of Strategists

The Trump administration has systematically dismantled the structures whose function was to foresee the consequences of their actions.

The closure of USAID is not just a humanitarian disaster - it is also the dismantling of the U.S. early-warning system for famine, disease, state collapse, and the resulting migration flows. For many years, USAID’s analysts were the U.S.’s best source of information on what was happening in the Sahel, Sudan, Yemen, and Bangladesh.

The State Department’s Africa Bureau has been downsized. Intelligence briefings are not being read. NSC positions are filled with loyalists instead of professionals.

Inspectors General fired in 2025 across twelve departments simultaneously - the officials tasked with identifying administrative consequences internally.

Public Integrity Section at the DOJ reduced from 36 lawyers to 2.

FCPA enforcement suspended by executive order - the removal of oversight mechanisms against corruption.

Each individual removal is justified by a local logic (cost-effectiveness, deep state, inefficiency). The cumulative effect is that the U.S. government has lost its ability to see itself. Decisions are made without impact assessments. The war on Iran is launched without anyone in the room able to answer what it will mean for Somali bread prices. USAID is being shut down without anyone being able to answer how many refugees this will generate in 18 months.

It is the butterfly effect in reverse: not that small actions have major consequences, but that major actions are taken as if they were small, because the system for assessing consequences has been dismantled.

This is not a hypothetical warning. It is an already documented series of defeats. Krugman summed it up on May 11: experts warned that tariffs would raise consumer prices without bringing back jobs - it happened. Experts warned that Hegseth’s “warrior ethos” and purge of those with doubts about loyalty would weaken the military in war - it happened. Experts warned that the Iran attack would lead to quicksand and a global energy crisis - and it did. Experts warned that Trump’s threats against allies would undermine American credibility - and it did. Inflation is rising. Industrial employment is falling. The Strait of Hormuz is closed. As Krugman put it, Trump is now traveling to Beijing as a beggar, to ask China for help in getting out of his Iran mess. The experts were right. But the system that needed to hear them had removed them.

Friction is Feedback: Europe, Allies, and the New Breakthrough

How often have we in Europe been mocked by the U.S. for our slowness? Bureaucracy is friction, and friction is the enemy. Regulated states are stagnant. European institutionalism is portrayed as a museum piece, not as an engine.

“Move fast and break things.” “Get things done.” “America gets stuff done while Europe debates.”

Trump’s voters find him decisive, decisive. He gets things done. It is precisely this “speed is strength” narrative that is being celebrated. But what those same voters will experience in two or three years, when the credit card bill can’t be paid, when gas prices have doubled, when their pension fund has been halved - are the consequences of precisely this lack of friction.

Speed without a system of consequences does not generate decisiveness. It generates damage that only becomes visible afterward - sometimes long afterward. Just look at Reagan’s and Thatcher’s disconnects.

American decisiveness is not strength. It is the absence of the apparatus that would have spotted the error while it could still be corrected.

Europe’s institutions are criticized for being slow. But slowness is not failure - slowness is the time during which a state can reflect on itself. A system that has eliminated its own slowness has not gained speed. It has lost the ability to navigate.

The institutions of many European nations were deliberately built in response to the experience of fascism that struck the continent in the 1930s and 40s. The German Grundgesetz of 1949 contains so-called “perpetuity clauses” (Ewigkeitsklausel), which make certain fundamental rights impossible to repeal - even through constitutional amendment. The European Court of Human Rights. EU competition law. The Danish constitutional principle of separation of powers. The French Conseil Constitutionnel. All of these are institutions deliberately designed to make it difficult for a democratically elected leader to suddenly concentrate all power - because we have seen what happens when the checks and balances are absent.

Europe still has its institutions. They need to be made more efficient - not dismantled. The trend toward American-inspired dismantling exists - Orbán (former Hungarian leader), Meloni in certain respects, populism’s general frustration with the EU’s “slowness.” “ If we accept the American narrative that speed is strength, we’ll end up in the same place.

The European project isn’t perfect. But its slowness is its immune system.

Friction isn’t the enemy. Friction is feedback. When institutions are frictionless, they aren’t effective - they’re blind.

The consequences of the U.S.’s treatment of allies: the quiet breakup

While this essay was in the works, something happened that will have far greater structural consequences than the Iran war, than the asset price bubble, than the OBBB tax cuts. The U.S. is losing its allies. Not because allies have chosen it. But because the Trump administration has chosen it for them.

It started with Trump’s threats to “take” Greenland from Denmark - a NATO ally. It continued with tariffs against Canada, Mexico, and the EU. With pressure on Japan and South Korea to pay more for U.S. bases. With the threat to suspend Spain from NATO following its criticism of the Iran war. With Trump’s public accusation that NATO is a “paper tiger.”

The result is a coordinated movement that the American press is largely ignoring, but which the Danish, French, and German press are reporting as their top story:

On digital sovereignty, France has announced the phasing out of American video conferencing software (Microsoft Teams, Zoom) in the public sector by 2027 and its replacement with the French-developed Visio platform. Denmark’s Ministry of Digitalization has been in the process of replacing Microsoft Windows and Office 365 with Linux and LibreOffice since June 2025. Caroline Stage Olsen, then Minister of Digitalization, articulated the rationale clearly: “We want to be independent of the big tech companies and ensure digital sovereignty.” Germany (Schleswig-Holstein, ZenDiS, OpenDesk), Austria (the military), the Netherlands, Lyon, and a long list of European municipalities are following the same trend. The International Criminal Court in The Hague has switched from Microsoft Office to the German OpenDesk - after Microsoft closed Chief Prosecutor Karim Khan’s Outlook account in May 2025, following Trump’s sanctions against him.

On November 18, 2025, the French and German governments met at a joint Summit on European Digital Sovereignty. They launched a joint task force set to report in 2026. The Atlantic Council called it “Europe’s digital declaration of independence.”

This channels a significant amount of money away from U.S. tech companies.

On defense: The Wall Street Journal reported in April 2026 that European NATO members are actively working on a backup plan in case the U.S. withdraws from the alliance. A “EuroNATO” or “European pillar” within NATO is no longer a theoretical concept. It is in concrete planning. Germany has increased its defense budget to historic levels. Poland, Sweden, Finland, Norway, Denmark, and the Baltic states are establishing joint procurement structures. EU Article 42.7 - the mutual defense clause in the EU Treaty - is now being discussed as a possible NATO substitute. NATO’s former Secretary General Anders Fogh Rasmussen has publicly stated that “ Trump’s decisions are leading to the collapse of the alliance.”

The U.S. Pentagon’s own 2026 Defense Strategy, published in January, articulated this as policy: Europe is no longer a priority theater for American conventional primacy. Europeans are described as “rich, capable, and therefore responsible” for handling the Russian threat themselves.

Apart from the fact that the U.S. president is simultaneously threatening the Danish prime minister over Greenland.

On trade and the economy: Under tariff pressure, Canada and Mexico have accelerated their trade diversification away from the U.S. Australia has increased its trade cooperation with the EU and Japan. India is following the same trend. The BRICS bloc (Brazil, Russia, India, China, South Africa, plus new members) is now building real alternative payment systems that reduce dependence on the dollar. Reuters reported that the U.S.’s global reputation has fallen below Russia’s in 2026 international opinion polls.

This is the quiet upheaval. This is what the U.S.’s allies do not say out loud, because they still trade with the U.S., still cooperate militarily, still try to maintain formal relations. But beneath the surface, the movement is in full swing: We are becoming independent of the U.S. because the U.S. can no longer be trusted.

The deepest point is that American strength was never military or economic alone. It was based on alliances. A city on a hill, that the world would follow. When Trump dismantles the alliances - through insults, through tariffs, through threats, through public mockery - he is dismantling precisely what made the U.S. a superpower in the first place. He leaves the country economically large, militarily still powerful—but strategically isolated.

It is a process that cannot be reversed quickly. Once France has built Visio, they won’t go back to Microsoft Teams. Once Denmark has migrated its public sector to Linux, it won’t go back to Windows. Once Europeans have built their own defense structures, the need for American leadership will cease.

The U.S. is losing its geopolitical position at the same pace as its asset prices are rising.

The Course of the Tsunami

The cascades are not parallel. They are linked.

First wave (already underway): Oil prices hit poor importing countries first. The Philippines, Pakistan, Bangladesh, Nepal, and Zimbabwe are in an acute energy crisis. Fertilizer hits food production with a 6-12-month delay. According to the UN, a continued disruption of oil supplies through mid-2026 will lead to 32 million people in poverty and 45 million in extreme hunger.

Second wave (6-24 months out) : Migration flows. When USAID funds run out, food prices have risen 40-120% in certain markets, and public finances in low-income countries collapse under the weight of oil bills, movements begin. From the Sahel toward the Mediterranean. From Central America toward the U.S. From Southeast Asia toward Australia. Europe is the logical destination for large numbers. Political consequences in Europe: a further shift to the right, EU tensions over burden-sharing, and the undermining of the remaining liberal-democratic structures.

Third wave (12-36 months): Financial adjustment. If just one of the four assumptions collapses definitively - chip supply, energy, the dollar’s status, institutional predictability - asset prices will converge toward reality. A 40-50% correction from Buffett’s 230% above the historical average would hit U.S. pensions, Danish pensions, and global balance sheets. It will not be localized. The U.S.’s weight in global asset portfolios is too great.

Fourth wave (24-60 months): Geopolitical realignment. If Taiwan slips under Chinese control - through quarantine, coercion, or direct conflict - the technological and economic center of gravity will shift. The Western system, which has dominated since 1945, has lost its foundation of power without fighting for it.

Who chose the blindness